1) QE makes interest rates go up

I wrote an entire article about this common misunderstanding but I’ll give the Tl;Dr version here.

When the Fed does QE it inspires confidence in the market. Investors and large institutions understand that since the central bank is providing a liquidity backstop the risk of financial Armageddon is low. With the Fed at their back investors move further out on the risk curve in search of yield. Along the way they sell their safe and boring Treasuries, and this cumulative selling pressure far outweighs any purchase that the central bank is making. The result? Yields rise.

Conversely, when the Fed is not engaged in QE investors perceive higher risks in the market. Without central bank liquidity to keep the system running smoothly the chance of something going wrong is heightened. As such, investors sell some of their riskier assets and increase their holdings of Treasuries. That buying pressure drives down yields, hence why yields can fall when the Fed stops doing QE.

This is a well-documented phenomenon, even if it runs counter to the mainstream narrative about how central bank bond buying affects interest rates.

2) The dollar is a network not a currency

You hear it all the time: king dollar is dead. The Federal Reserve is going to do so much QE that it’s going to hyperinflate the dollar and we’re all going to be using gold by the end of the decade.

What most people fail to understand is that the United States dollar is more like Facebook than gold. The dollar is a network of commercial banks, computer systems, nostro and vostro accounts, Eurodollar money lenders, degenerate FX traders, cultivated relationships, Fortune 500 companies and central banks working in unison to keep our global financial system operating relatively smoothly.

People stay on Facebook even if it’s not their favorite platform because everyone else they know is on Facebook. There are better managed currencies than the dollar but no other currency has the dollar’s network effect.

No matter how much the Fed prints in the short term or what crazy policies the American government enacts, most of the world is going to continue using the dollar for the time being. There is currently no competition to the dollar’s complicated network of banking institutions, debt holdings and other financial instruments.

Will the dollar system ever end? Yes, nothing lasts forever. However the dollar’s death will happen slowly over the course of several decades, not overnight.

3) Just because interest rates are low that doesn’t that the economy is on fire

How often have you heard that the Fed has over-stimulated the economy by keeping interest rates at 0%? It’s basically conventional wisdom at this point, but this idea deserves some pushback.

The level of interest rates is only one half of the equation. To understand the complete picture we also have to consider the availability of credit. Who has access to those 0% interest rates? If rates are at zero but banks aren’t lending money into the real economy, then the stimulative effects are low. In fact history has proven that many banks would rather lend to other financial institutions, which can lead to asset price inflation rather than headline inflation.

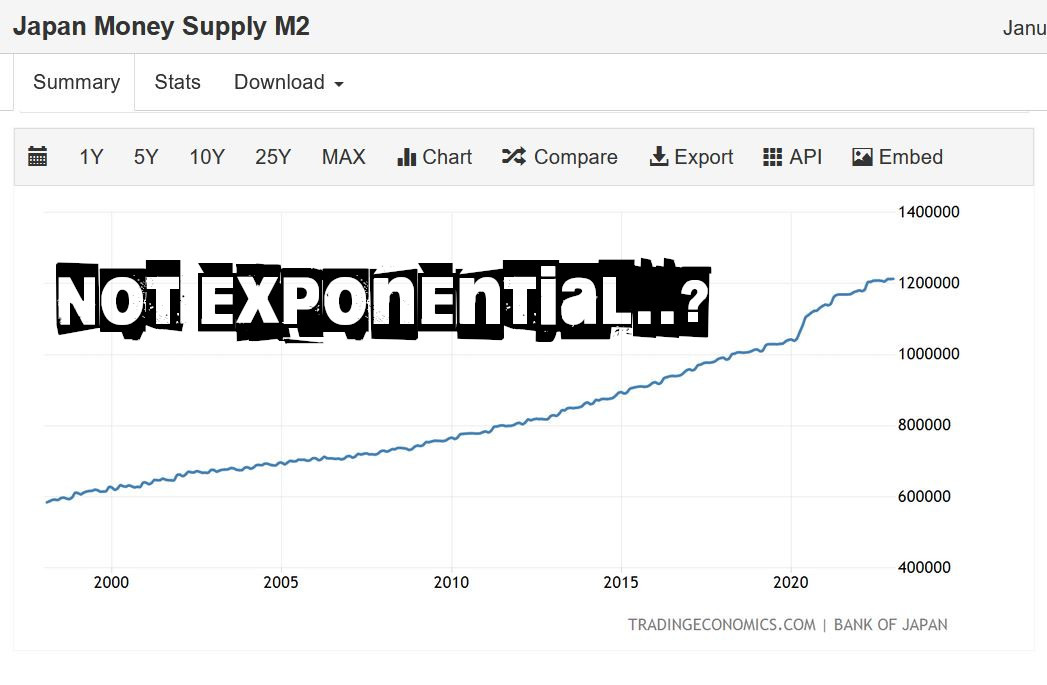

Also, when rates are low all across the yield curve it means that investors are parking their money in bonds. This is risk-off behavior that’s not at all indicative of an economy that’s running red hot. As a general rule, nations with 0% interest rates do not have a fantastic economy. See Japan as a prime example…

4) We have a debt refinancing system, not financing system

We like to think of the financial and banking system as a tool that entrepreneurs and businesses can use to grow their operations. Among many other things, banks finance new businesses right? Well, not so much… In his book Capital Wars (which I reviewed here), Michael Howell has pointed out that because of the trillions of dollars of debt that already exists, we no longer have a debt financing system instead we have a debt refinancing system. Here’s a quote from the book.

“The fact that the modern financial system has turned from a new financing system to a refinancing system that is more than ever dependent on the supply of potentially flaky safe assets to help rollover increasingly flaky debts creates a negative feedback that highlights the inherent dangers in credit markets.”

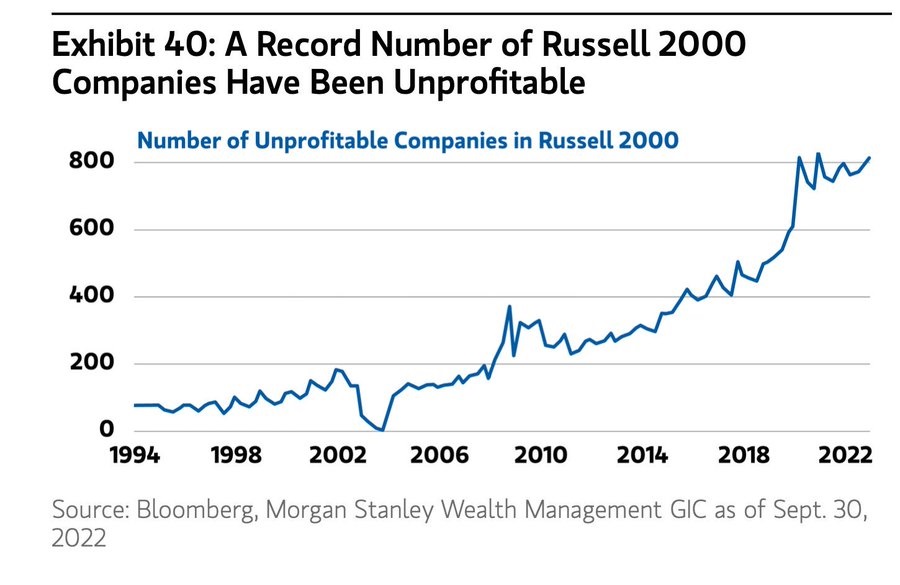

Howell estimates that a majority of all debt transactions are refinancing as opposed to new financing. The implications are profound. New debt is (semi) optional. A business can choose to put off an expansion or an entrepreneur can (hopefully) wait six months to get financing. However, debt refinancing is not optional. Approximately 40% of the companies in the Russell 2,000 are unprofitable which means that if they can’t roll over their debt at an affordable rate, those businesses will go bankrupt.

Notice that keyword, “affordable rate.” Higher rates can be especially damaging to an over-indebted economy like ours, which is one of the reasons that central banks are playing with fire every time they raise rates. If companies can’t get access to the credit markets to refinance their bonds, the economic devastation is going to be immense.

5) The Fed can’t define money

We often talk about M2 as if that measurement encapsulates the real money supply. Unfortunately, it does not. In fact we only use M2 because we have no other alternatives. Thanks to the Eurodollar system (and other factors) not even the Federal Reserve knows how much money is really in circulation. Here are two simple examples.

1) US Treasuries are pristine collateral in the Eurodollar system and these Treasuries collateralize trillions in dollar loans. Treasuries are money-like and have a direct impact on dollar supply, but they’re not counted by M2.

2) The stablecoin USDT Tether has a market cap of $70 billion. A drop in the bucket to be sure, but USDT is widely circulated as a dollar substitute yet it’s not counted in M2 money supply.

As an investor it’s important to understand that M2 is only an approximation and does not give us a very detailed accounting of how many dollars are actually out in the system. Here’s another quote from Michael Howell illustrating this point.

“It is our contention that ‘modern money’ really starts where conventional definitions of money supply end. In other words, the well-known monetary aggregates, e.g. M0, M1 and M2, are only the tip of the growing iceberg of short-term claims that, as the 2007-2008 GFC shows, can severely disrupt the markets.”

6) There isn’t a direct connection between QE and money supply

The mainstream media loves to talk about QE as money printing, however, there’s not actually a direct connection between quantitative easing and the amount of money in the system.

When the Fed does QE they create bank reserves and use them to buy Treasuries from large banks like Goldman Sachs and JPMorgan. At this stage QE is more of an asset swap than anything, since the Fed is merely trading bank reserves for Treasuries.

For QE to increase the money supply the large banks would need to lend against their bank reserves. Whether they choose to do so is entirely at the bank’s discretion. If banks don’t want to lend then it doesn’t matter how much QE the central bank does, the money supply won’t increase.

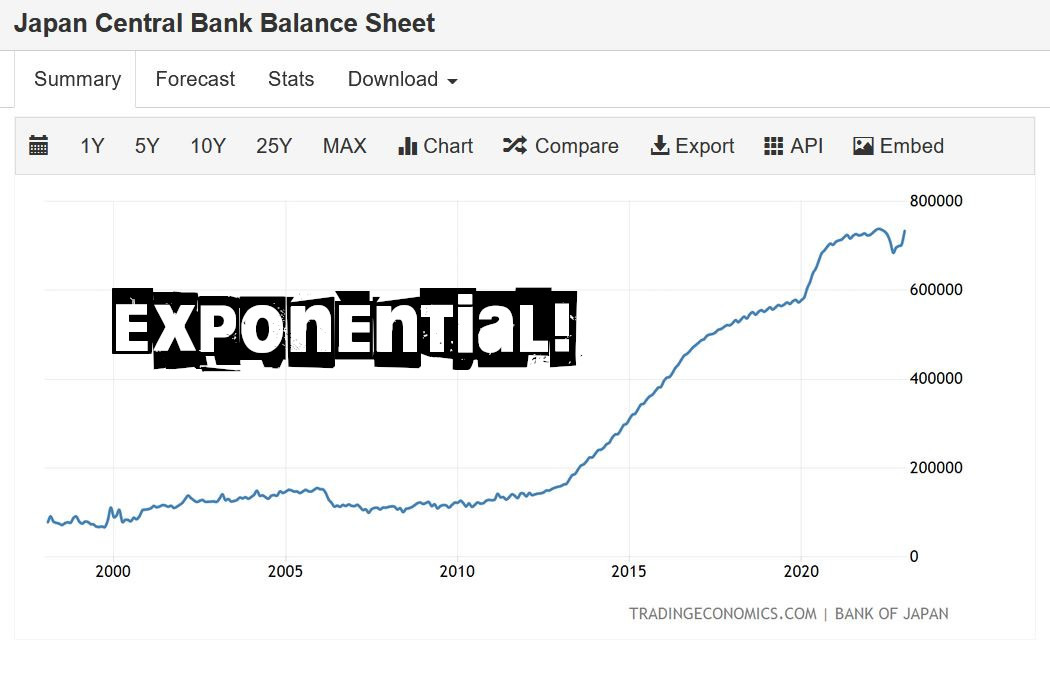

Japan provides us with a great example of this phenomenon. In these two charts we can see that the BOJ’s balance sheet has gone parabolic in the last decade while Japan’s money supply has only grown at a modest rate.

7) We are in a silent depression

Hugh Hendry and Emil Kalinowski have both argued that the United States is in a silent depression. What does that even mean? It means that the United States is well below the trend rate of growth from previous decades.

The financial system has never recovered from 2008 and has failed to generate the type of economic investment and expansion that people have come to expect. Ben Hunt has done some excellent work showing how we’ve tried to paper over this lack of growth by expanding the money supply and going into debt, but this can only go on for so long.

Even if most people can’t identify the factors contributing to a silent depression, they can feel the effects. Sluggish wage growth, lack of economic opportunity, rising levels of political polarization as we try to deal with a perceived feeling of loss. Fixing our financial system may in fact be the first step towards creating a better, less divided society.